Share via

The foundation of your payment setup rests on a key distinction: Aggregation (also known as Payment Facilitation or PayFac) vs. Direct Merchant Accounts (often referred to Independent Sales Organisation or ISO at Peach Payments).

Think of it like a business deciding how to set up shop in a bustling market. Do you rent a stall in a big, established food court, or do you build your own stand from the ground up? The first is a lot quicker to get up and running, while the second gives you more control. This is the fundamental difference between these two models for accepting electronic payments.

Aggregation Merchant Account (Payment Aggregator)

This model is a simplified, “plug-and-play” approach. In this model, Peach Payments acts as a ‘super-merchant,’ onboarding businesses (sub-merchants).

How it works:

- Aggregation merchants use Peach Payments as an intermediary to settle transactions. Peach Payments handles the contractual relationship with the payment method provider or acquirer, meaning the merchant does not have a direct agreement with them. This distinction affects various aspects of transaction processing, including reconciliation and settlement references. Within this model, chargebacks are also handled by Peach Payments.

- A single, large merchant account is created by a payment service provider – in this case Peach Payments. This provider then allows thousands of small businesses (called “sub-merchants”) to use their master account to process payments. When a customer pays a sub-merchant, the money goes into the aggregator’s account first, and then the aggregator pays out the funds to the business’s bank account.

Key Characteristics:

- Ease of Setup: The primary benefit is speed. A business can often sign up online and start accepting payments within one to three business days

- No Individual Merchant ID: The business does not get its own unique Merchant ID (MID). It operates under the aggregator’s MID.

- Limited Customization: These accounts offer less flexibility in terms of reporting, settlement schedules, and advanced features.

- Merchant Transaction Limits: In respect of card transactions, merchants on our aggregator account have set transaction caps. Once these limits are reached, we must move them to their own ISO MID for compliance and smoother processing.

Current limits:

- Visa: USD 1,000,000 per merchant

- Mastercard: USD 10,000,000 per merchant

- Absa discretionary: USD 4,000,000 per merchant

Hitting these thresholds reflects merchant growth and unlocks benefits of a dedicated ISO MID with tailored processing and settlements.

*Certain industries are prohibited from being on aggregation. Our experts are able to advise accordingly.

Direct Merchant Account (ISO – Independent Sales Organisation)

This is the traditional, more “bespoke” model for payment processing. In this model, Peach Payments provides technical services for payment integration, but the merchant establishes a direct contractual relationship with the payment provider for settlement and billing.

How it works

- With a Direct Merchant Account, merchants have a direct agreement with an acquiring bank or payment provider, and their transactions are settled directly by that entity. Peach Payments integrates these payment methods, providing the technical infrastructure for processing.

Key Characteristics:

- Rigorous Underwriting: The process is more involved. The business must go through a formal underwriting process with the payment method provider, which includes credit checks, a review of business history, and an assessment of risk. This can take several days or even weeks.

- Individual Merchant ID: Each business gets its own unique Merchant ID (MID). This provides more control and security.

- Customized Pricing: The rates are negotiated based on factors like industry, transaction volume, and average ticket size.

- Lower Risk of Account Holds: Since the account is dedicated to a single business, funds are not held or affected by the actions of other companies. Holds on funds are less common and are typically tied to the specific business’s activity.

- Greater Control and Features: Dedicated accounts often come with more advanced features, customized reporting, and better integration options with business software.

Summary of Key Differences

This is the traditional, more “bespoke” model for payment processing. In this model, Peach Payments provides technical services for payment integration, but the merchant establishes a direct contractual relationship with the payment provider for settlement and billing.

| Feature | Aggregation Merchant Account | ISO Merchant Account |

| Setup Process | Fast and easy (minutes/hours) | Slower, formal underwriting (days/weeks) |

| Merchant ID | Shared with other sub-merchants under Peach Payments’ master account | Unique and dedicated to the business |

| Pricing | Simple, flat-rate model | Customized and tiered rates (often lower for high volume) |

| Funds Control | Funds flow through Peach Payments’ settlement account first before payout to the merchant | Funds go directly to the merchant’s account |

| Best For | New, small, or low-volume businesses; startups; businesses that prioritize speed and simplicity over cost | Medium to large businesses; established businesses; those with high-risk needs or complex processing requirements or a preference for a direct contractual relationship with the payment provider. |

For a CEO, the choice between these two models is a strategic one that depends on the current size and future plans of their online store. A startup might begin with an aggregation account for the speed and simplicity, but a growing, established business should consider transitioning to a dedicated Direct Merchant Account to gain more control, lower costs, and reduce risk.

Learn more about Payments 101. Read our blog on 3RI next.

Scale with Peach

Learn how we help scale some of Africa's most exciting businesses

Business tips, case studies, interviews with online store owners and business trends…

The New Standard for Payouts in South Africa

Peach Payments and Yoyo add bank card-linked loyalty to Digit Pro POS device

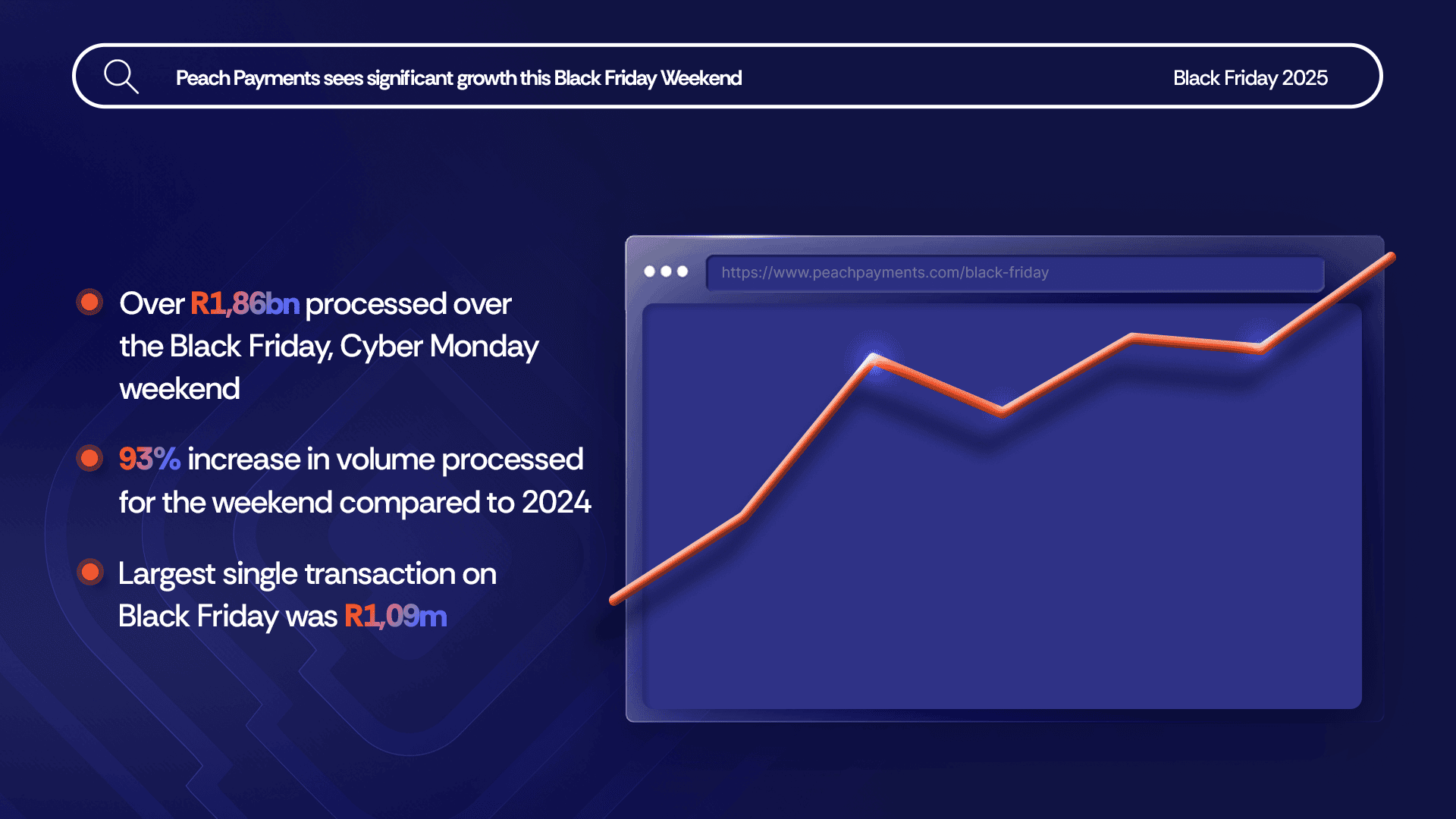

Black Friday up 93% over 2024, R1,86bn processed

Bringing Our New Peach Values to Life

Samsonite in-store payment methods

How global and regional companies can use the Mauritius IFC to centralise online payments and treasury functions

# PeachFriday Merchant Deals 2025

A merchant’s guide to chargebacks

Four Black Friday payment realities for merchants

What are Direct Merchant Accounts (ISO) versus Aggregation Accounts?

What Is 3RI? Everthing you need to know about Requestor-Initiated Authentication

Highlights from the 2025 World Wide Worx Online Retail Report

What is Interchange? Everything you need to know about interchange fees

Cadana Pay x Peach Payments: Unlocking seamless global Payouts

Peach Payments announces real-time clearance Payouts

Peach Payments x MoneyBadger partnership goes live

Peach Payments launches enterprise-level POS terminal

iTickets x Peach Payments Point of Sale

Peach Payments x Digicape: Powering Premium Apple Experiences with Seamless Payments

Peach Payments acquires West-African payments gateway PayDunya

Navigating International Transactions

Seize the Sale with Buy Now, Pay Later

2024 Wrapped: A Year of Innovation and Growth at Peach Payments

RCS payment option now available through Peach Payments

Peach Payments sees impressive growth this Black Friday Weekend

#PeachFriday Merchant Deals 2024

Your Ultimate Guide to Payment Security for Black Friday

Scaling with Peach Payments: Unveiling the Product Roadmap

Scaling with Peach Payments: Revolutionising Reconciliation

Scaling with Peach Payments: The Future of Payments