3D secure is a security protocol that adds a layer of authentication to the online payment experience by verifying a cardholder’s identity when they are using their card details instead of swiping with their actual card. The purpose is to protect a customer’s card against unauthorised use when shopping online.

The first iteration of 3DS appeared in 1999. Card networks like Visa (Verified by Visa) and Mastercard (Mastercard Identity Check) implemented this feature in 2001. In the first iteration, customers needed to authenticate themselves using OTP or One Time Password.

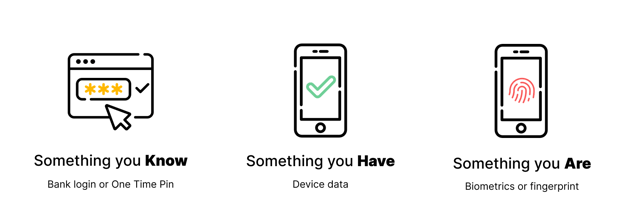

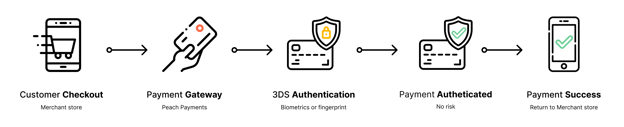

To authenticate the customer is usually required to provide something they have (device), something you know (One Time Pin), or something you are (Biometrics – like a fingerprint)

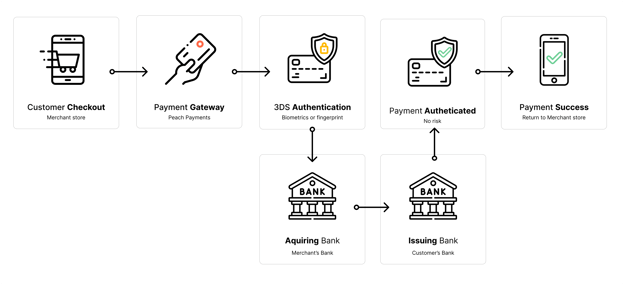

3DS involves three domains: the acquiring bank (or the merchant’s bank), the issuing bank (or the cardholder’s bank), and the infrastructure supporting this protocol, such as Peach Payments.

3DS 1.0 promised to help prevent fraud by shifting the burden of authentication onto the issuers (Customer’s bank). This led to a huge loss in false declines as customers would choose to cancel a transaction when seeing a 3DS pop-up (or more likely a redirect) to avoid any potential fraud.

So what does 3DS look like?

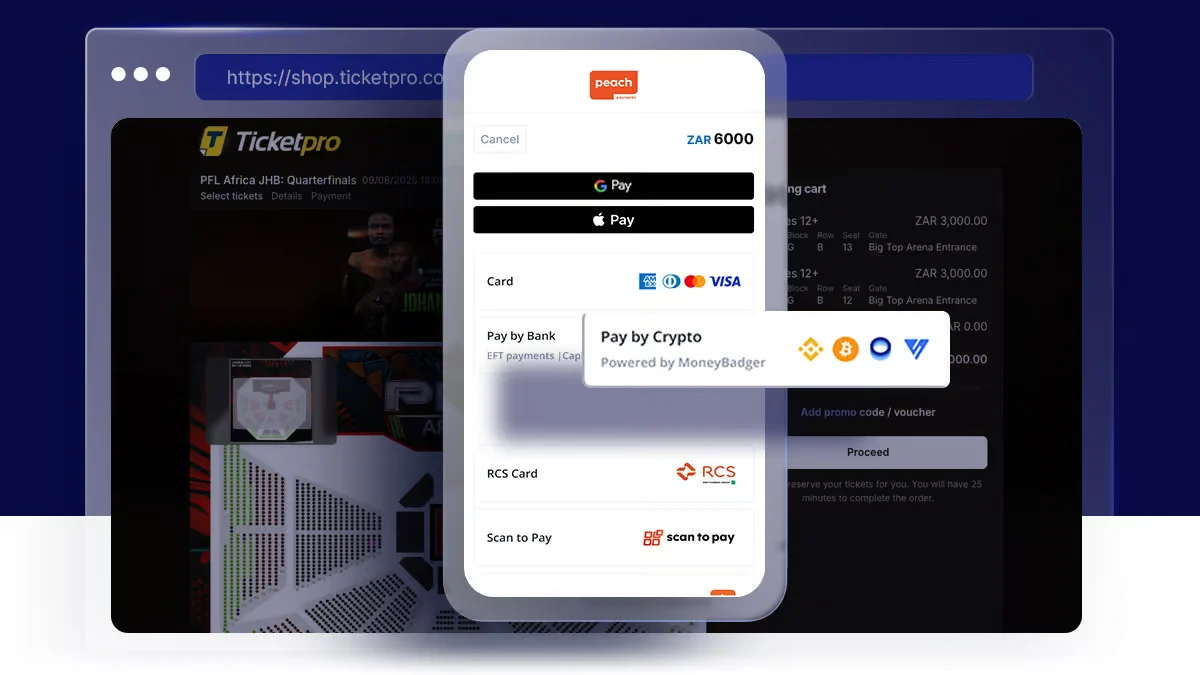

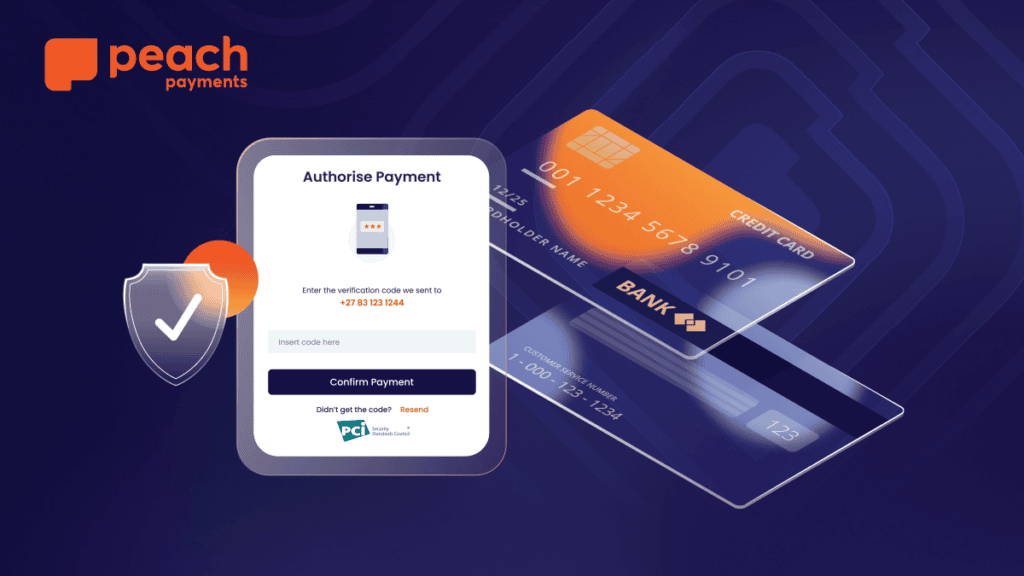

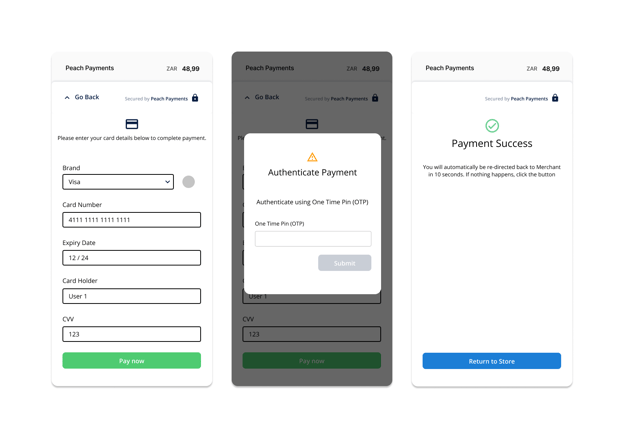

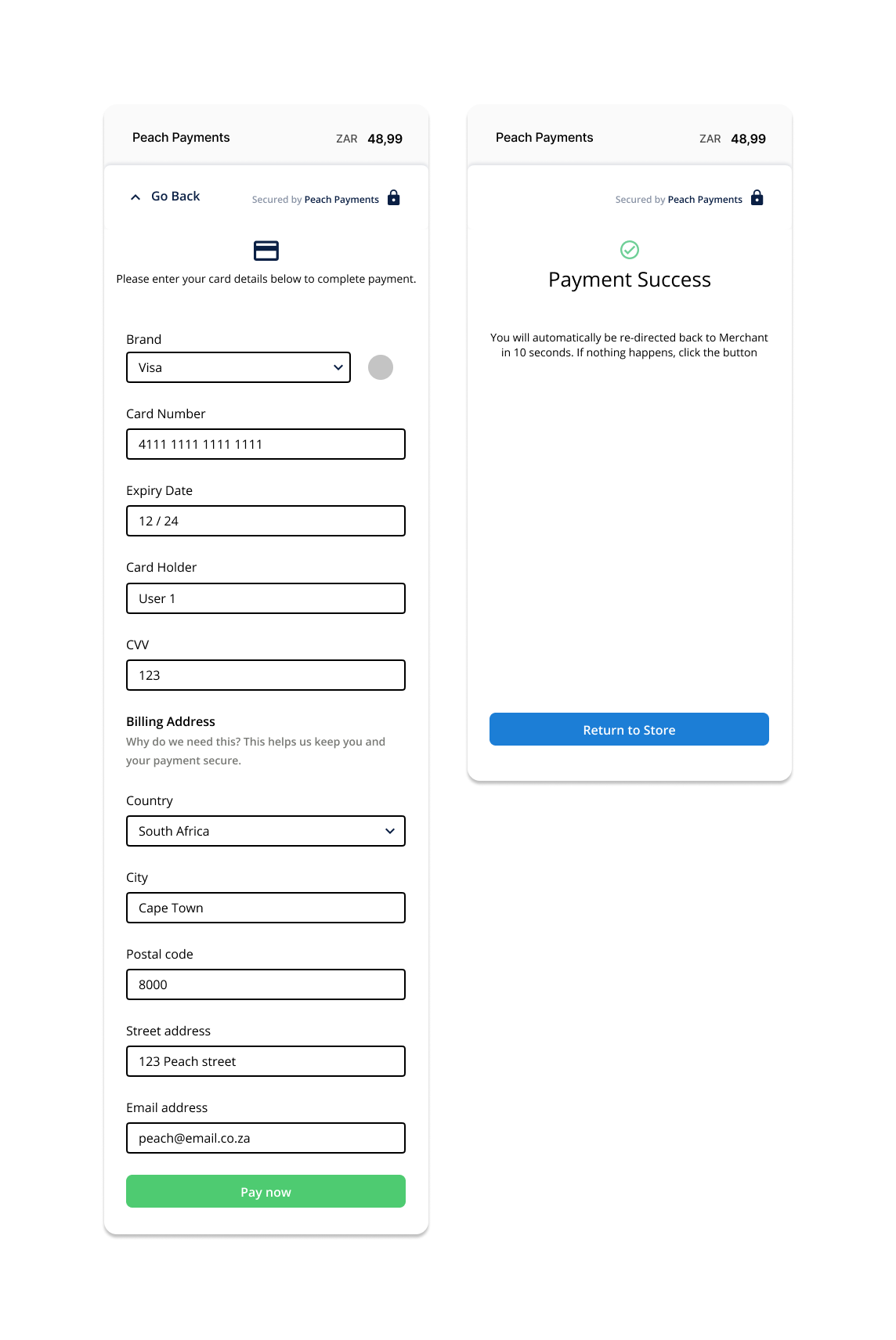

You know when you buy something online and a little pop up appears asking you to enter an OTP or approve your purchase in your banking app? Yup, that’s 3DSecure in action.

What improvements are found in 3D Secure 2.0?

3DS 2.0 offers additional fraud protection by analysing information about the customer and prompting them to verify their identity when making a high risk transaction. By assessing the customer’s information and the risk of their transaction, customer’s may not have to verify their identity to authenticate every transaction they make.

What does it look like? No extra steps, no pop ups and no OTP or fingerprint needed!

When a transaction is trusted the customer will continue on the frictionless flow (No OTP or Biometrics required to authenticate)

If a transaction is deemed suspicious or high-risk, the customer is then required to authenticate (OTP or Biometrics) in the challenge flow.

What is risk-based authentication?

Risk-based authentication is the process of determining the risk attached to a particular transaction and, based on that risk level, whether or not the customer should be challenged.

The risk-based assessment includes:

- The value of the transaction

- New or existing customer

- Transactional history

- Behavioural history

- Device information

- Shipping Address

- Billing Address

What does this mean for Peach Merchants?

Peach Merchants are not required to make any changes, although they do have the option to submit additional data related to customers and transactions to further improve their customer’s online purchasing experience.

So should you? It has been shown that 3DS 2.0 can increase conversion rates by almost 8%, reduce false declines and is overall a better checkout experience.

Additional data points:

- Account Type

- Address Match Indicator

- Browser IP Address

- Cardholder Billing Address

- Cardholder Email Address

- Cardholder Home, Mobile, Work Phone Number

- Cardholder Name

- 3DS Requestor Non-payment Indicator

- Cardholder Shipping Address

- DS Reference Number

- EMV Payment Token Indicator

- SDK Encrypted Data

- Transaction Type

- 3DS Requestor Challenge Indicator

- 3DS Server Operator ID

- Cardholder Account Identifier

Conclusion

Peach Payments will be supporting 3DS 2.0 by 31st October 2021 and will be expecting all Merchants to support 3DS 2.0 by 31st October 2022 as 3DS 1.0 will no longer be supported by our banks.

Peach Payments is always looking to improve our product and customer experience. 3DS 2.0 is the next step in fraud prevention and a big leap in improving the customer online purchasing experience, and upping your business’s conversion rate.