Share via

In Part 1, we covered how building a robust pan-African payments business is not for the faint hearted. Complexity comes with growth and businesses looking for a payment gateway provider that alleviates the stress of scaling their business across products and regions don’t need to look much further. We’ve constantly solved for Africa’s biggest problems around fragmentation. Part 2 covers how we do this.

From Moving Money to Orchestrating Scale

The broader payments industry is currently trapped in what I call the “race to zero.” Competitors are slashing transaction fees in a desperate bid to win market share, treating payment processing as a basic utility, much like electricity or water. At Peach Payments, we believe that while payments is utility at the pure processing level – there is an inherent complexity and opportunity to differentiate at the layers above, especially with the integration of a robust payment gateway.

Utilising a payment gateway can streamline this process, allowing businesses to focus on growth and customer satisfaction while reducing operational complexities.

As an enterprise client this can mean accessing new customers, new countries and more importantly improving conversion rates which will more than compensate for any short term gain from a cheaper basic processing solution. This realisation has driven our strategic pivot from being a company that simply “moves money” to one that “orchestrates scale”.

We have introduced an updated Payment Orchestration Layer, which serves as the central nervous system for an enterprise’s financial operations. Rather than a linear path from merchant to bank, orchestration allows for:

- Rule-Based Routing: The system can automatically decide, in milliseconds, which bank or processor is most likely to approve a specific transaction at the lowest possible cost i.e. balancing the trade-off between conversion and cost.

- Failover Redundancy: In the African context, “uptime” is a relative term. Banks go down, and telecommunications links fail. Our orchestration engine provides instant redundancy. If one provider fails, the traffic is immediately re-routed to a secondary or tertiary provider. The merchant stays live, the customer remains happy, and the revenue is secured.

This leads to our “Open Kitchen” philosophy. Most payment providers treat their internal processes as a black box. You put a transaction in, and hopefully, money comes out the other side. We take the opposite approach. We want our enterprise partners to see the “messy innards” of tax laws, fraud vectors, and local regulatory requirements. By providing this level of transparency and visibility, we prove our value as an architect. We handle the complexity so that the merchant can focus on their core ambition: growth.

Building Resilient Code: Security, AI, and Network Tokenisation

As we look toward 2026, the definition of “resilience” in fintech is evolving. It is no longer enough to be secure; you must be proactive.

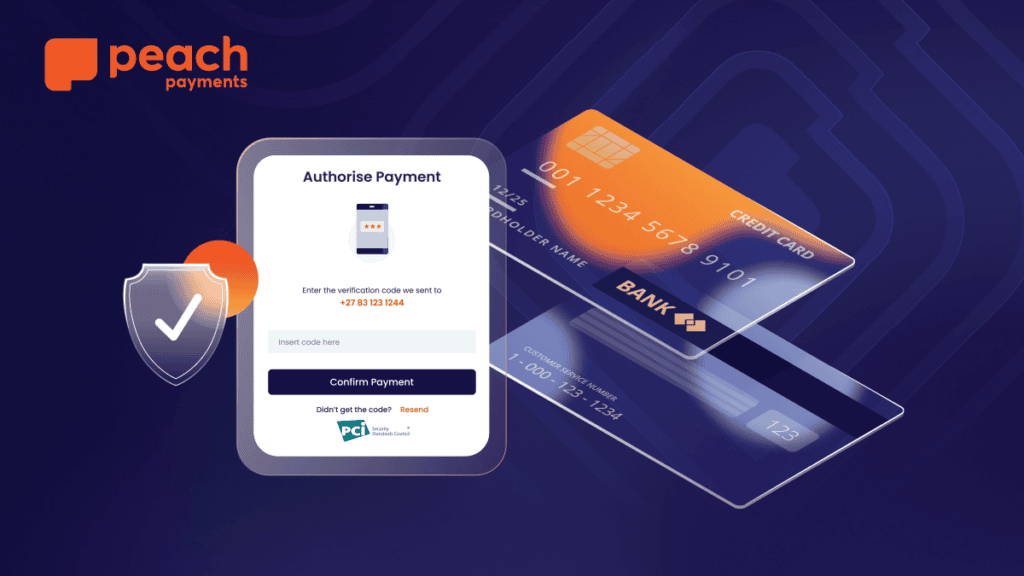

One of our most significant technical levers is Network Tokenisation. At the core of this is a unified token strategy, where Peach Payments provides merchants with a single, PCI-compliant token that represents a customer’s payment credentials. This token can be safely stored and reused across channels (web, mobile, recurring billing), which removes the need for merchants to handle sensitive card data directly and significantly reduces PCI scope.

More importantly, it solves the problem of “involuntary churn”. For subscription-based businesses, like the home cleaning or meal kit services we partner with, an expired credit card usually means a lost customer. With network tokenisation and built-in lifecycle management, the token remains valid even if the physical card is replaced, ensuring the billing cycle remains uninterrupted.

Regarding the opportunities of Artificial Intelligence, my perspective is built-on 2 pillars – consumer behavior and risk management. There is no doubt that consumer behavior is evolving and that AI will fundamentally affect digital commerce. On the risk front, we believe AI governance belongs in the CISO’s (Chief Information Security Officer) office. We don’t use AI just to generate marketing copy. We use it for proactive threat modeling. In a continent where fraud patterns can shift overnight, AI allows us to identify and neutralise sophisticated fraud vectors before they impact our merchants’ bottom lines.

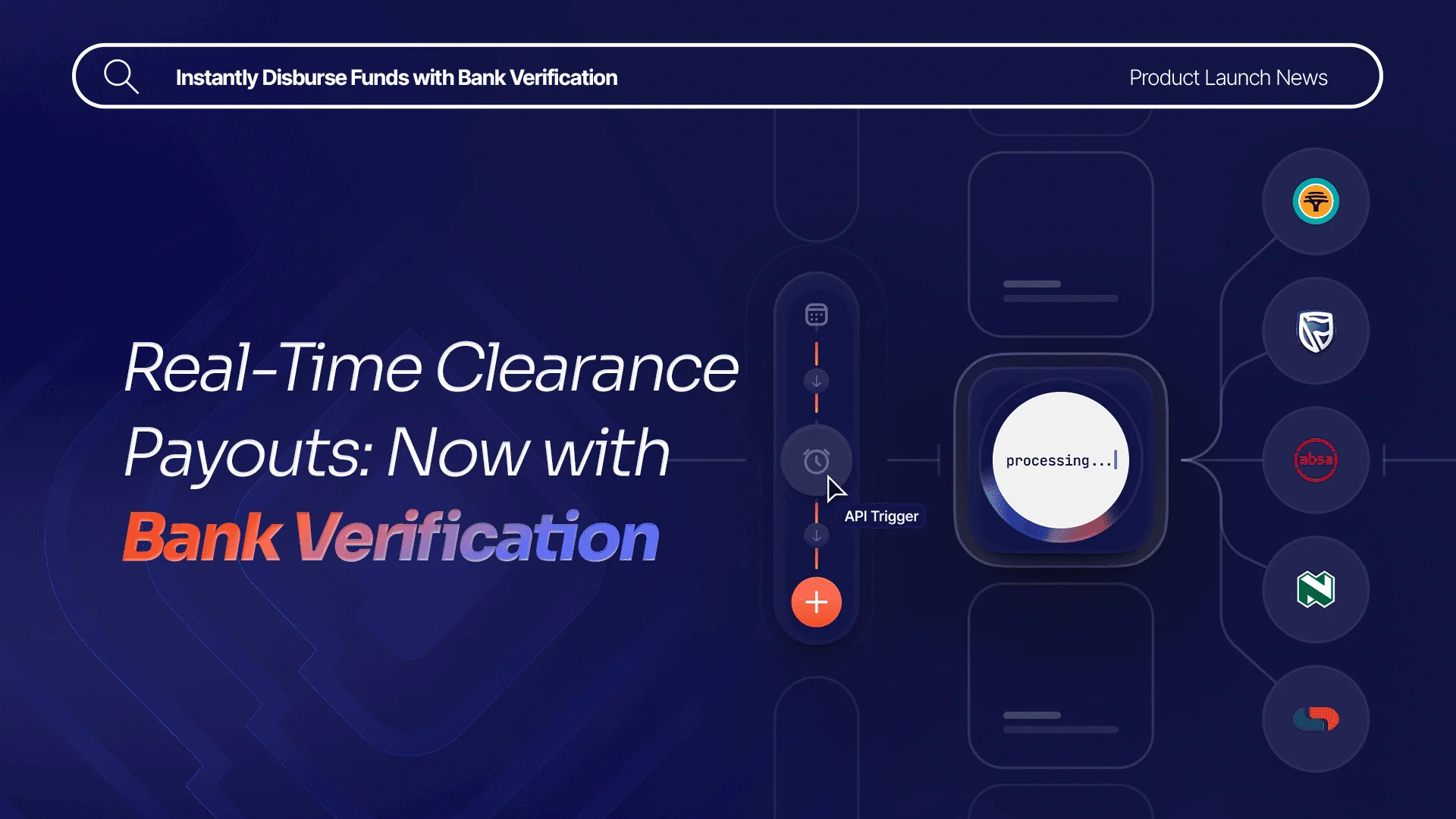

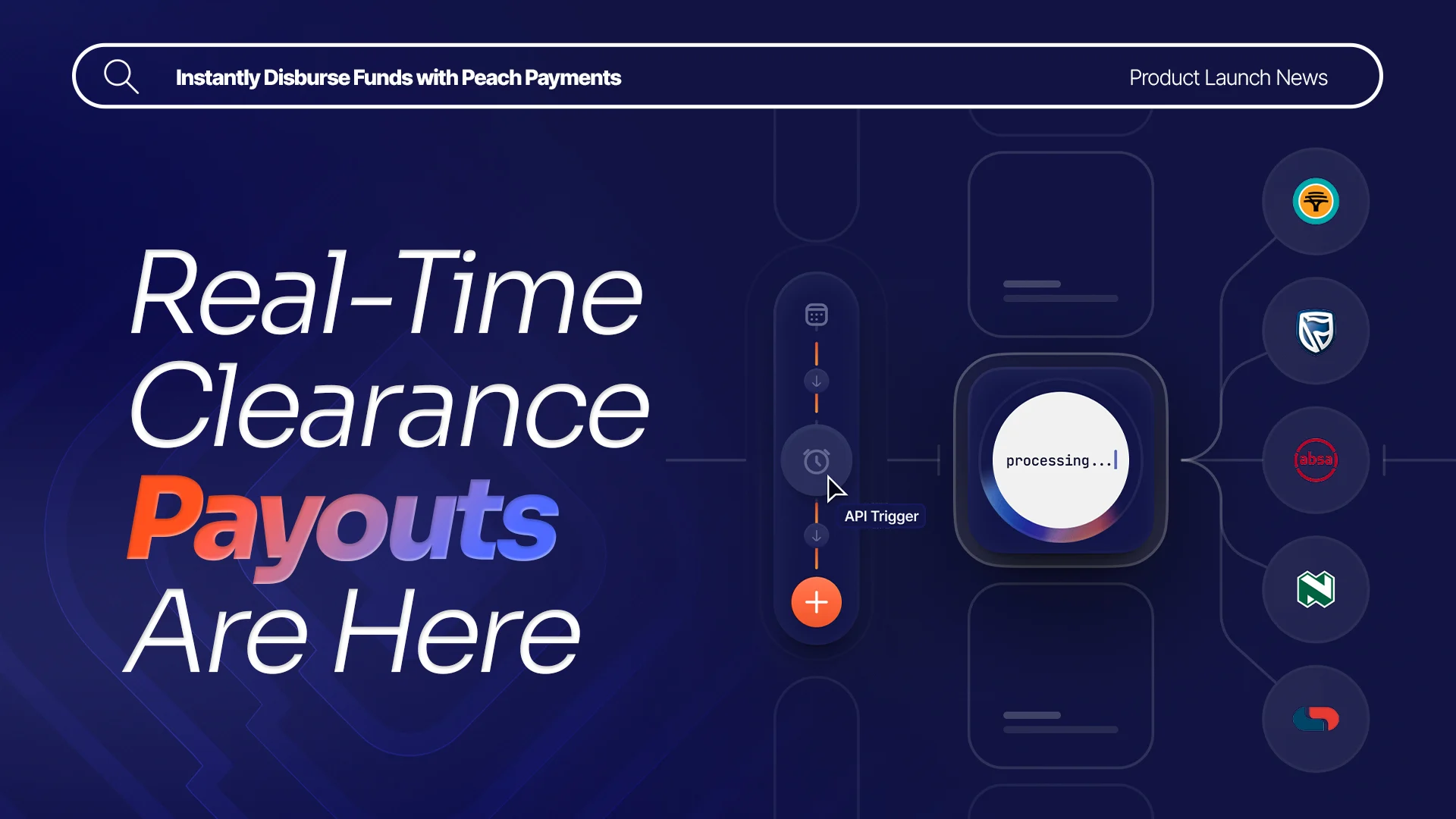

Furthermore, a system is only as strong as its weakest link. That’s why real-time payouts with bank verification is a gamechanger. The goal is to ensure that every pay-out is verified before a single cent moves. By confirming account ownership and details in real-time, we eliminate the administrative nightmare of failed disbursements and the catastrophic risk of man-in-the-middle fraud.

Conclusion: Complexity. Solved.

At the end of the day, our brand promise is captured in two words: Complexity. Solved. To be clear, “Solved” does not mean the complexity of the African market has been eliminated. The capital controls are still there, the currencies are still volatile, and the regulations are still fragmented. What “Solved” means is that this complexity has been engineered, contained, and stress-tested by an architect.

We provide our partners with what we call “earned calm”. It is the peace of mind that comes from knowing your payment infrastructure is as ambitious as your business plan. For the enterprise leader, the message is simple: Stop looking for a tool that promises to make Africa look easy. Start looking for an architect who knows exactly why it is hard—and has built a system to thrive in it anyway.

First published in the Business Day Payments, May 2026.

Scale with Peach

Learn how we help scale some of Africa's most exciting businesses

Business tips, case studies, interviews with online store owners and business trends…

Solving complexity: Part 2 - The Strategic Pivot

Solving complexity: Part 1 - The Irony of Progress

Retail & E-Commerce payments—The Conversion Engine

Travel & Hospitality Payments - Fly me to the boom

Five payment pain points hotels face and how to solve them

Giving your customers the ultimate checkout shortcut with Embedded Express

PayJustNow on Peach Payments’ POS device improves in-store payment experience

Peach Payments brings Apple Pay to merchants

From Check-in to Check-out

How Multiple Payment Options Improve Online Travel Sales

The New Standard for Payouts in South Africa

Peach Payments and Yoyo add bank card-linked loyalty to Digit Pro POS device

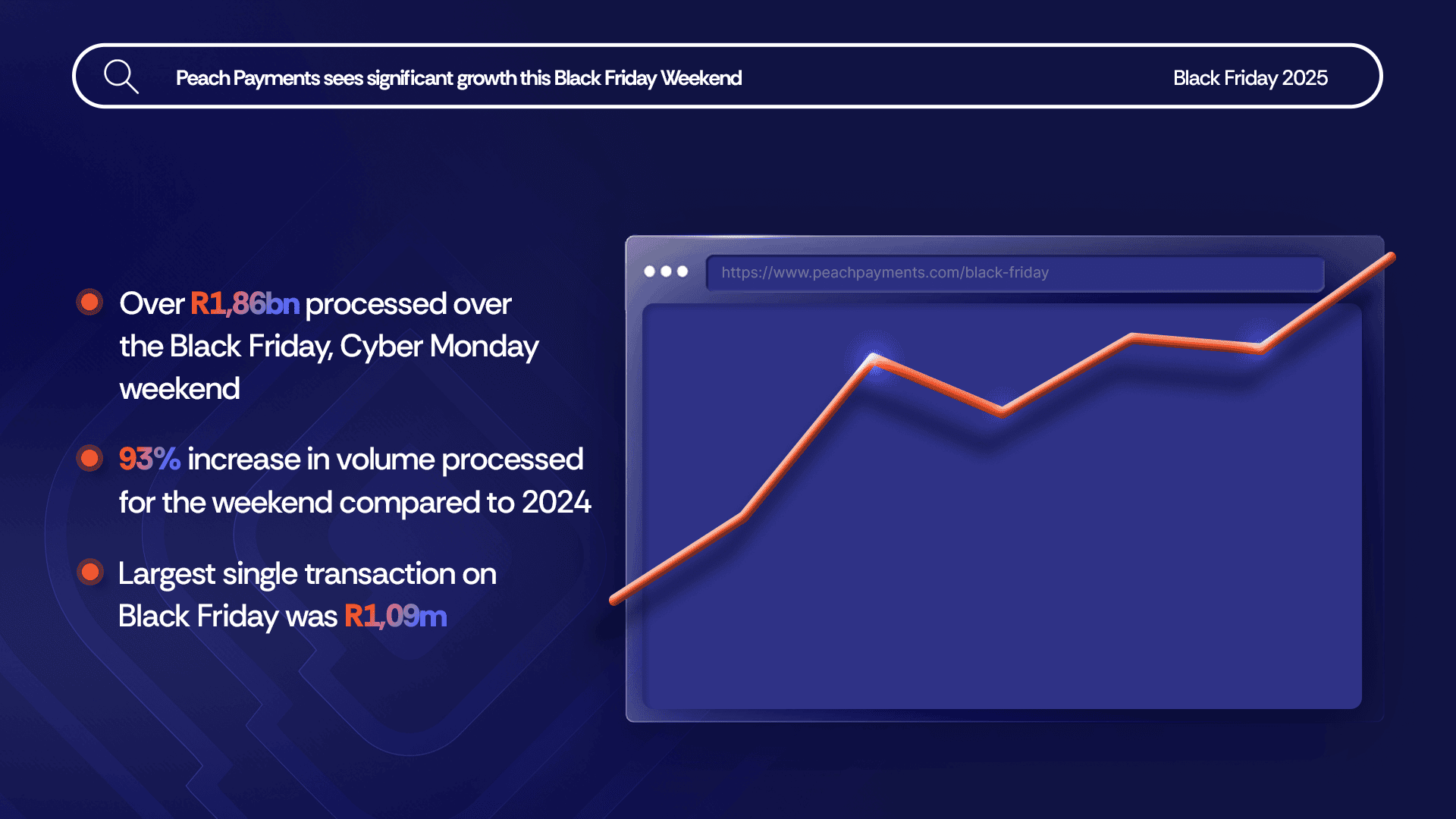

Black Friday up 93% over 2024, R1,86bn processed

Bringing Our New Peach Values to Life

Samsonite in-store payment methods

How global and regional companies can use the Mauritius IFC to centralise online payments and treasury functions

# PeachFriday Merchant Deals 2025

A merchant’s guide to chargebacks

Four Black Friday payment realities for merchants

What are Direct Merchant Accounts (ISO) versus Aggregation Accounts?

What Is 3RI? Everthing you need to know about Requestor-Initiated Authentication

Highlights from the 2025 World Wide Worx Online Retail Report

What is Interchange? Everything you need to know about interchange fees

Cadana Pay x Peach Payments: Unlocking seamless global Payouts

Peach Payments announces real-time clearance Payouts

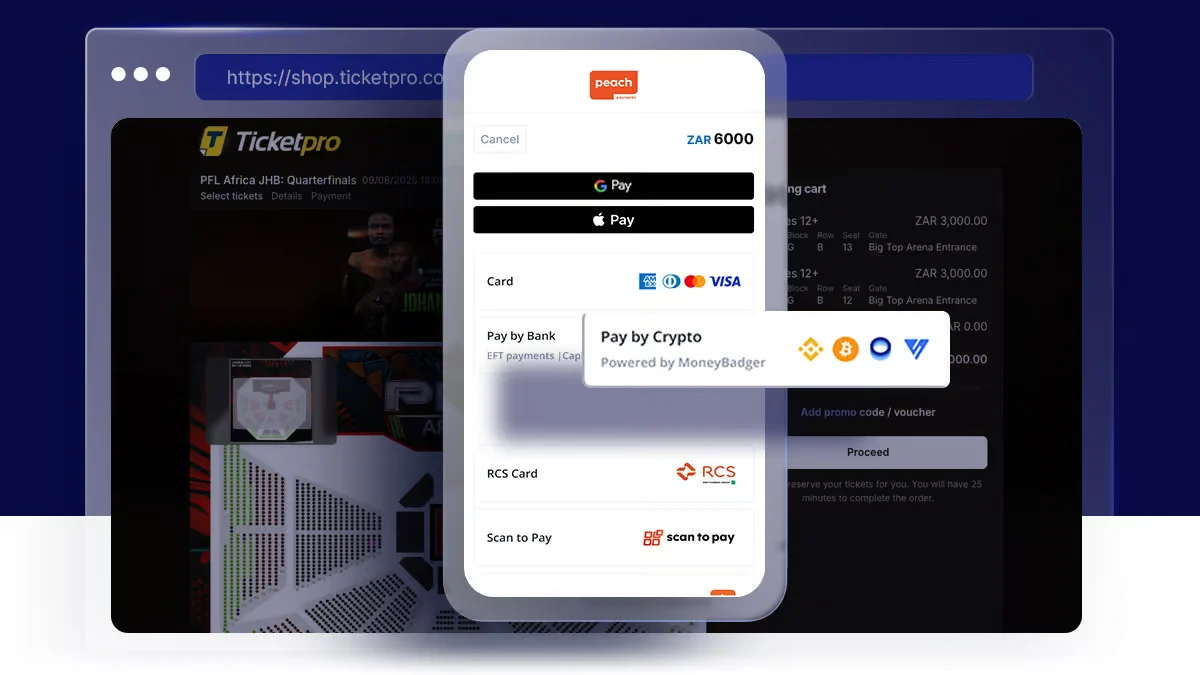

Peach Payments x MoneyBadger partnership goes live

Peach Payments launches enterprise-level POS terminal

iTickets x Peach Payments Point of Sale

Peach Payments x Digicape: Powering Premium Apple Experiences with Seamless Payments

Peach Payments acquires West-African payments gateway PayDunya